CBAM: What exporters need to do now to stay compliant with eu carbon rules

The eu carbon border adjustment mechanism (cbam) is changing how carbon-intensive goods are traded into the european union. It is designed to apply a carbon price at the border that reflects the emissions embedded in imported products, aligning the carbon cost of imports with what eu producers face under the eu emissions trading system (eu ets).

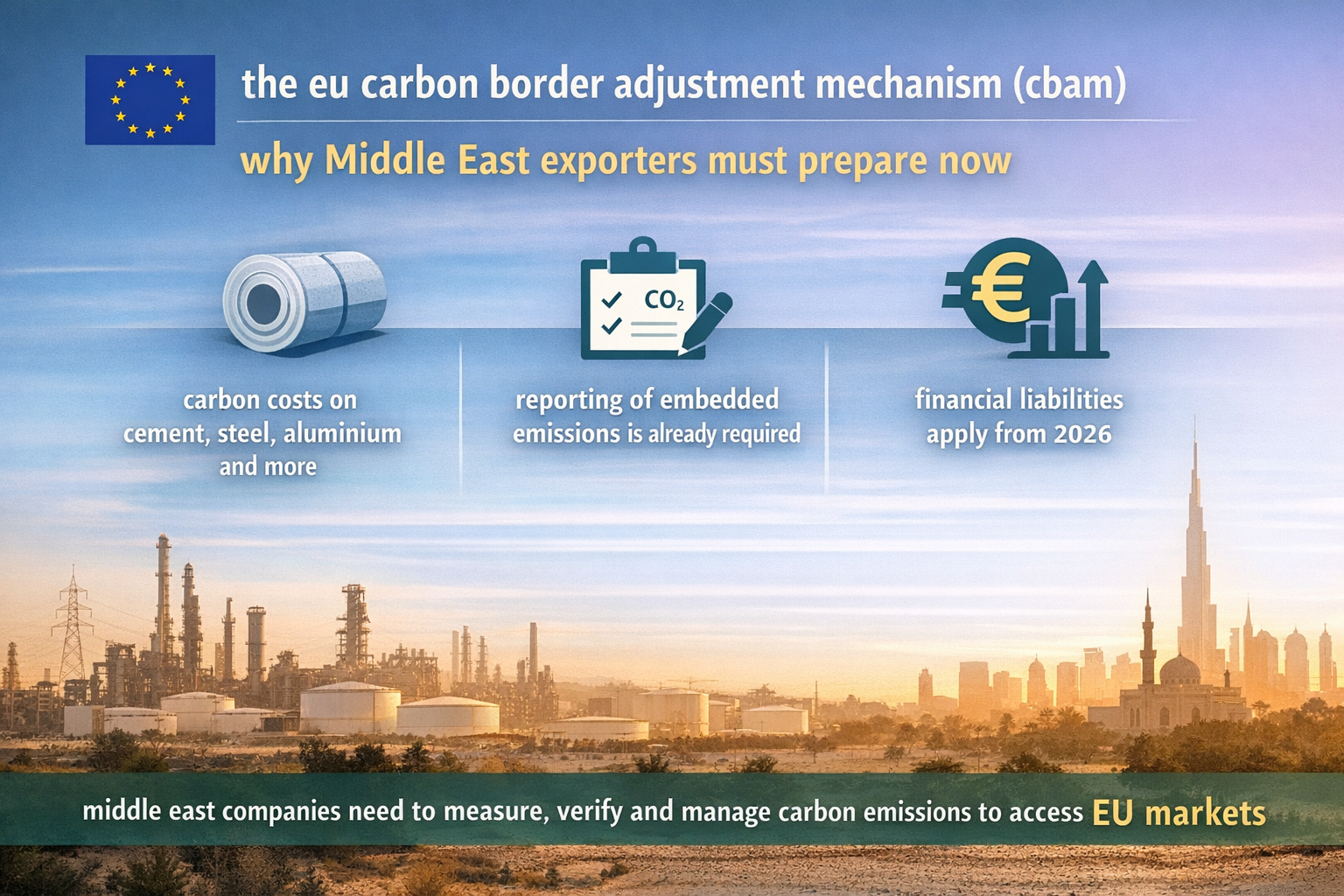

For many middle east countries and exporters, cbam is not an abstract policy issue—it affects market access, pricing, contracts, and customer relationships with eu buyers. The key shift is that embedded emissions data becomes a trade requirement, and from 2026 it becomes a direct cost driver through the purchase and surrender of CBAM certificates.

This article explains what cbam is, what changes in 2026, what middle east companies need to do to comply, and how building robust emissions data systems is quickly becoming a competitive necessity.

What cbam is (and why it exists)

Cbam was introduced to address carbon leakage—the risk that production shifts to jurisdictions with weaker carbon constraints, or that eu manufacturers lose competitiveness to higher-carbon imports. The mechanism aims to put a “fair price” on the carbon emitted in producing certain imported goods, while encouraging cleaner production in non-eu countries.

Cbam also aligns with the eu’s broader climate policy direction, including the gradual phase-out of free allowances under the eu ets for sectors at risk of carbon leakage. In other words: cbam and the eu ets are increasingly designed to work together—one pricing carbon inside the eu, the other addressing carbon embodied in imports.

Which products are in scope

Cbam initially covers imports in six high-emissions sectors (defined via product codes in the regulation’s annex):

- cement

- iron and steel

- aluminium

- fertilisers

- electricity

- hydrogen

For middle east exporters, this scope is especially relevant because several regional economies have strong export positions in aluminium, iron and steel products, fertilisers, and energy-related value chains. The commercial consequence is straightforward: if your product is in scope (by cn code), cbam compliance becomes part of doing business with eu customers.

Which products are in scope

Cbam initially covers imports in six high-emissions sectors (defined via product codes in the regulation’s annex):

- cement

- iron and steel

- aluminium

- fertilisers

- electricity

- hydrogen

For middle east exporters, this scope is especially relevant because several regional economies have strong export positions in aluminium, iron and steel products, fertilisers, and energy-related value chains. The commercial consequence is straightforward: if your product is in scope (by cn code), cbam compliance becomes part of doing business with eu customers.

Timeline: transitional reporting (2023–2025) vs definitive regime (from 2026)

Cbam was introduced with a transitional phase from 1 october 2023 to 31 december 2025, where the core obligation is reporting embedded emissions (rather than paying). The definitive regime starts 1 january 2026, when importers must hold and surrender CBAM certificates corresponding to the embedded emissions of goods imported.

This “report first, pay later” design was intended to allow supply chains time to build emissions measurement capacity. But 2026 marks a clear line: companies that have not established reliable product-level emissions data risk disruption—through defaults, disputes with customers, higher effective carbon costs, or compliance delays.

Who is responsible: eu importers, but exporters must provide the data

Legally, cbam obligations sit with eu importers (or indirect customs representatives), who must become authorised cbam declarants and manage reporting and certificates. However, the required emissions information typically comes from the non-eu producer (operator) side of the supply chain.

This means middle east producers will increasingly be asked—by eu customers, procurement teams, and auditors—to provide installation-level emissions, clear system boundaries, and documentation that stands up to verification. In practice, exporters that cannot provide credible emissions data will face commercial pressure, even if they do not file cbam declarations themselves.

What “embedded emissions” means under cbam

Cbam is built around the concept of embedded emissions—the greenhouse gas emissions associated with producing the imported goods. The core rules are set in the cbam regulation and further detailed in implementing rules on calculation methods.

A key compliance point: embedded emissions can include direct emissions from production processes and, where applicable, indirect emissions from electricity used in production. The applicable calculation approach is formalised through implementing regulations that lay down methods for calculating emissions embedded in goods, aligned with eu ets methodology foundations.

For exporters, the operational takeaway is that cbam reporting is not a generic corporate footprint. It is product- and installation-specific—and must be calculated using methods that align with the eu’s cbam framework. [eur-lex.europa.eu], [taxation-c….europa.eu]

What happens from 2026: certificates, pricing, and cost exposure

From 1 january 2026, cbam moves into its definitive regime: eu importers will need to purchase cbam certificates and surrender them annually based on the emissions embedded in their imports. Certificate pricing is linked to the eu ets allowance price (calculated as an average—quarterly in 2026 and weekly from 2027 onward, according to commission guidance).

A critical commercial detail: if an importer can prove that a carbon price has already been paid in the country of production, an equivalent amount may be deducted from the cbam obligation—subject to the eu rules. That makes credible documentation of any local carbon costs and the underlying emissions calculation even more important.

For middle east exporters, cbam should therefore be treated as both:

- a compliance obligation (data, methods, evidence), and

- a pricing and competitiveness variable (carbon intensity becomes part of the product’s cost narrative in eu markets). [taxation-c….europa.eu], [kpmg.com]

What middle east companies need to do to comply (a practical checklist)

Below is a practical, non-theoretical roadmap that middle east producers and exporters can start implementing immediately.

step 1: confirm whether your products are in scope (by cn code)

Cbam scope is determined by product classification (cn codes) listed in the regulation’s annex, not by marketing description. Many “downstream” and “selected” products can also be included depending on classification.

action: map your exported products (and any relevant precursors) to cbam scope codes and confirm with customs specialists where needed. [eur-lex.europa.eu], [taxation-c….europa.eu]

step 2: define your installation boundaries and data owners

Cbam compliance relies on installation-level emissions data, so companies need clarity on:

- what constitutes the “installation”

- which processes are included

- who owns data (operations, energy, finance, sustainability)

- how evidence is stored and approved [eur-lex.europa.eu], [clcouncil.org]

action: create a documented boundary and responsibility matrix before you start calculations.

step 3: build monitoring, reporting and verification (mrv)-ready data

Cbam is increasingly “mrv-like” in practice. The eu has issued implementing rules that set methods for calculating embedded emissions, building on eu ets approaches.

action: implement controls around activity data (fuel, process, electricity), emission factors, metering, and reconciliation to production outputs—so results are repeatable and auditable. [eur-lex.europa.eu], [taxation-c….europa.eu]

step 4: decide when to use actual data vs defaults (and understand the risk)

Where actual data is unavailable, cbam allows the use of default values under defined conditions and implementing frameworks. However, defaulting can be commercially disadvantageous if default values are higher than your actual emissions intensity, or if buyers demand verified actuals to manage cost exposure. [taxation-c….europa.eu], [ey.com]

action: prioritise actual data for your highest-volume or highest-margin eu product lines first. [taxation-c….europa.eu], [ey.com]

step 5: align cbam data with customer requests and contract language

Because the legal obligation sits with the eu importer, exporters should expect new contract clauses such as:

- requirements for timely emissions data delivery

- audit rights / verification requirements

- liability sharing if data is missing or incorrect

- pricing adjustments linked to certificate cost exposure [taxation-c….europa.eu], [clcouncil.org]

action: prepare a standard “cbam data pack” and internal governance workflow so commercial teams are not reinventing responses per customer. [clcouncil.org], [taxation-c….europa.eu]

step 6: quantify financial exposure and reduce emissions strategically

Cbam turns emissions intensity into a market signal. The ability to reduce direct emissions (efficiency, electrification, process optimisation) and manage indirect emissions (electricity sourcing strategy where applicable) can materially affect competitiveness over time. [taxation-c….europa.eu], [kpmg.com]

action: treat CBAM as a driver for investment-grade decarbonisation planning, not just reporting. [kpmg.com], [taxation-c….europa.eu]

Common pitfalls we are seeing

Even companies that take cbam seriously can run into predictable issues:

- treating cbam as a corporate footprint exercise, rather than product and installation-level reporting [eur-lex.europa.eu], [eur-lex.europa.eu]

- poor traceability (numbers exist, but the evidence trail does not) [eur-lex.europa.eu], [clcouncil.org]

- late engagement with eu customers, leading to rushed data requests and default usage [taxation-c….europa.eu], [kpmg.com]

- no internal ownership across operations, sustainability and finance—creating inconsistent disclosures [clcouncil.org], [kpmg.com]

The underlying pattern is that cbam pushes organisations toward systems and governance, not only reports.

How sq impact can assist companies with cbam readiness (without replacing your experts)

Cbam compliance requires more than a one-off calculation. It requires a repeatable capability: consistent data capture, clear boundaries, traceable evidence, and outputs that can be shared reliably with eu importers and verifiers. The eu’s cbam framework is explicitly built on structured calculation methods and operational procedures for the definitive regime. [eur-lex.europa.eu], [taxation-c….europa.eu]

SQ Impact supports this kind of readiness by helping organisations move from fragmented spreadsheets and ad-hoc reporting to structured, governed data flows. Specifically, the platform can help in four practical ways:

1) centralising cbam-relevant activity data and evidence

Cbam calculations rely on granular inputs (fuel use, electricity use, production volumes, process data) and auditable documentation. sq impact can act as a central repository and workflow layer to keep data consistent, versioned, and attributable to owners. [eur-lex.europa.eu], [clcouncil.org]

2) structuring data to match cbam reporting logic

CBAM requires embedded emissions calculated under defined methods and presented in a way that supports declarations and verification. SQ Impact can help standardise boundaries, assumptions, and calculation-ready inputs across sites and product lines—reducing the risk of inconsistent reporting.

3) improving audit readiness through traceability and controls

Because cbam moves into a financial obligation regime from 2026, evidence quality and governance matter. sq impact supports audit-ready processes by linking metrics to sources, approvals, and change logs, supporting stronger assurance outcomes.

4) connecting compliance data to decarbonisation decision-making

Cbam is a price signal. Over time, companies that manage emissions intensity strategically will be better positioned competitively. sq impact can help translate emissions data into prioritised actions and tracking—so the organisation can reduce embedded emissions and improve its market position rather than only reporting them.

If you want to see how sq impact is structured for sustainability and carbon reporting workflows, you can explore the platform overview here: https://www.sustainquality.com/sqimpact/

Conclusion: cbam is a trade requirement—data capability is the differentiator

Cbam’s direction is clear: the eu is embedding carbon transparency into market access for carbon-intensive goods, with reporting obligations already in motion and financial liabilities in effect from 2026. [taxation-c….europa.eu], [eur-lex.europa.eu]

For middle east exporters, the companies that navigate this best will be those that:

- build reliable installation-level emissions data,

- create mrv-ready processes and evidence, and

- integrate cbam compliance with long-term decarbonisation strategy. [eur-lex.europa.eu], [kpmg.com]

In short: cbam is not just a reporting challenge. It is a competitiveness challenge—and a systems challenge.